What the Data is Showing Right Now

This is where it gets really interesting. The headline number is massive… but the rate of change matters more.

-

Total U.S. household debt: $18.8 trillion

-

Credit card debt: $1.28 trillion (record high)

- Quarterly increase: +$44 billion

These numbers aren’t just growing… they’re accelerating exponentially!!!

Let’s Zoom In Further

- ~46% of U.S. adults with credit cards are carrying a balance

-

Average interest rates: 20%+

- Many cards go well above 25%–30% APR

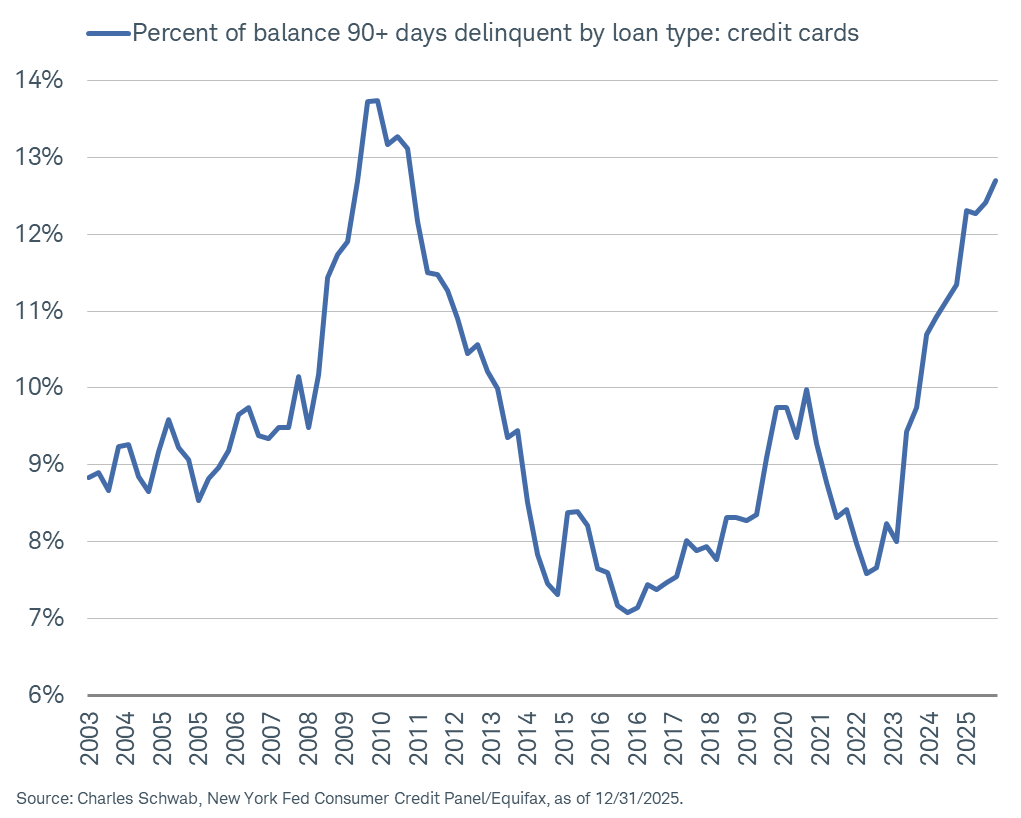

- Delinquency rates: 4.8% and rising

What stands out to me is how high these rates are going, and the usage is increasing.

When paired with compounding forces, this won’t stay linear for long.

The Curve We Need to Watch

If you map this out over time, something subtle, but powerful, starts happening.

Looking through time:

- Past: Credit used occasionally, paid off monthly

- Present: Credit used to smooth cash flow

- Future: Credit becomes a permanent layer of daily life

A major challenge in our economy is that costs are rising faster than income.

So people rely on credit to close the gap. Debt is no longer short-term...it’s sadly ongoing (and we see it in the numbers)!!!

Why This Is Actually Accelerating

This is the part I think most people underestimate.

This isn’t about spending more...it’s about a widening gap.

- Housing costs have doubled since 2018

- Car prices have doubled over the last decade

- Purchasing power has barely grown

Now add oil.

When oil rises, it increases the cost of EVERYTHING: Transportation, food, goods, and daily life.

Even if nothing major changes, your baseline cost of living increases.

That gap has to be filled somehow. Right now, that “somehow” is credit and CREDIT CARDS.

What starts as a short-term solution becomes a long-term system.

The Hidden Risk: Compounding at ~20%+

Here is where compounding flips amigos!

We talk a lot about compounding in investing at Angeles.

But this is the inverse.

At 20%+ interest:

- Time works against you

- Progress slows down

- Exit becomes harder

- DEBT COMPOUNDS

Here’s what most people miss!

Minimum payments create the trap.

They feel manageable… but barely touch the principal.

So:

- The balance doesn’t really go down

- Interest keeps compounding

- The timeline stretches out for years

Small balances don’t stay small.

They grow slowly. Then suddenly feels overwhelming.

This is exponential growth in reverse.

What This Means For YOU

We’re moving into a world of credit-backed consumption, where daily life is financed, pressure is persistent, and short-term debt becomes long-term dependency.

This is where you take control.

- Awareness is leverage: seeing the curve early changes how you act today.

- The cost of capital matters: At 20%+, debt is aggressive.

- Cash flow is king: Stability comes from control, not just income.

- Small decisions compound: What feels minor today can become major tomorrow.

My Leadership Insights

- We need to fix this, or there will be a permanent class of citizens in a debt trap.

- Financial literacy is vital. Understanding debt, interest, and capital is vital for consumers and businesses.

- Watch the policy shift. As pressure builds, watch intervention moves, potential rate caps, more regulation, and structural change.

Get Ready!!! Exponential Growth Is Here Too

Right now, this still feels manageable. That’s what makes it dangerous.

Exponential change doesn’t announce itself early.

It accelerates… then it becomes obvious.

By the time everyone sees it, the curve has already moved.

David Olivencia